ESRS for Non-EU Groups (N‑ESRS): What Your Group Needs to Know and Do

N‑ESRS is the EU’s new sustainability reporting standard that requires large non‑EU groups with significant EU turnover to disclose their impacts on people and the environment.

It will reshape sustainability reporting for large non‑EU groups active in the EU.

An estimated 1200 companies will be in the scope of N-ESRS:

- 350-450 USA

- 150-200 UK

- 100-150 Switzerland, Japan

- 20-50 Cayman Islands, China, Canada, Rep. of Korea

- 10-20 Brazil, Mexico, Hong Kong, India, Bermuda, Virgin Islands

The objective of your N-ESRS sustainability report, taken as whole, will be to present fairly all your group’s material sustainability-related impacts, and how it manages them (through policies, actions, metrics and targets), reported at a global level.

N-ESRS is an impact-only reporting standard – the EU cannot impose full financial risk reporting on non-EU parents, and the legal mandate (Article 40a) is impact focused – but there are benefits to applying full ESRS on a voluntary basis:

- If the non-EU ultimate parent company applies full ESRS, the CSRD in-scope subsidiaries of that non-EU company could benefit from subsidiary exemption. But only if the non-EU parent company applies full ESRS.

Timeline: What happens when

- Mid‑July 2026: Exposure Draft published by EFRAG

- Mid‑July – October 2026: Public consultation (100 days)

- Early June 2026: Call for interest to participate field test

- July – October 2026: Field tests with report preparers

- January 2027: EFRAG delivers technical advice to the European Commission

- Mid‑2027: N-ESRS adoption as delegated act

- FY 2028: First reporting year

- 2029: First N‑ESRS report published

Source : EFRAG SRB Online Meeting 3 June 2026, https://vimeo.com/event/5947235

-

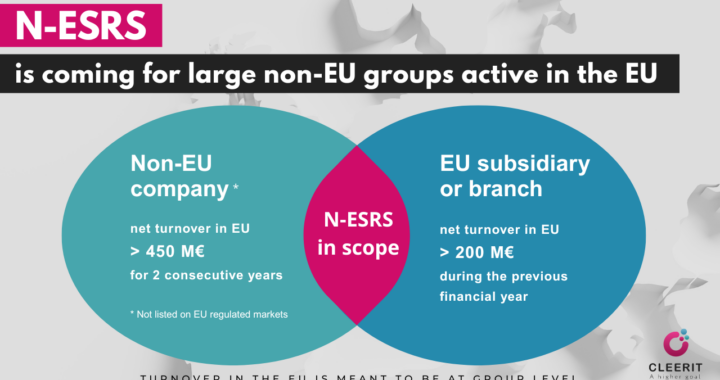

Who must report and when

Your group is in scope if it meets the both these two threshold criteria (Article 40a after Omnibus I):

- Criteria 1: EU turnover > EUR 450 million for two consecutive years (at group level)

AND

- Criteria 2: at least one EU subsidiary or branch with a net turnover in EU > EUR 200 million during the previous financial year

First reporting year: FY 2028, report published in 2029

-

What you must report

N‑ESRS is based on simplified ESRS, but focuses only on impacts, not financial materiality:

- Disclosures on risks, opportunities, financial effects, resilience and dependencies are removed.

- But financial information is per se strictly not excluded, it is needed to provide contextual information to understand impacts!

This is the core design choice: N‑ESRS = ESRS minus the financial‑materiality pillar.

Mandatory disclosure areas (Article 40a)

Strategy & business model

- Plans to align with 1.5°C and climate neutrality by 2050

- How stakeholder interests and sustainability impacts are considered

- How sustainability strategy is implemented

Governance

- Role, expertise and skills of administrative/management bodies in sustainability oversight

- Incentive schemes linked to sustainability matters

Policies

- Description of the group’s policies in relation to sustainability matters

Targets

- Time‑bound sustainability targets, including at least GHG targets for 2030 and 2050

- Progress toward targets

- Whether environmental targets are based on scientific evidence

Due diligence

- Description of due diligence process implemented by the group with regard to sustainability matters (aligned with EU requirements where applicable)

Impacts

- Principal actual and potential adverse impacts across own operations and value chain, including products and services, business relationships and supply chain

Actions

- Actions taken to identify and monitor those impacts, and other adverse impacts which your group is required to identify according to other EU requirements to conduct a due diligence process

- Actions taken to prevent, mitigate, remediate or bring to an end actual or potential adverse impacts, and the results of such actions

Indicators

- Metrics relevant to all disclosures above (governance, strategy, policies, actions, targets)

Topics covered

You must report across 12 standards (same structure as ESRS): Climate, pollution, water, biodiversity, circularity, own workforce, value‑chain workers, communities, consumers, business conduct, plus general requirements and disclosures.

-

What perimeter to use (global vs EU‑related)

You will choose between three approaches (no final drafting yet):

Option 1 – Global approach (default)

- Report global impacts for all topics.

Option 2 – Mixed approach (flexible by topic)

- Climate impacts: always global

- Other topics: option to report only EU‑related impacts, if:

- Impacts are managed separately (e.g., EU segment, EU products)

- EU‑related impacts include customer‑based and location‑based components

Option 3 – Full ESRS (voluntary)

- If the non‑EU parent applies full ESRS, EU subsidiaries may benefit from the subsidiary exemption.

-

Interoperability with IFRS S1/S2

The objective is to avoid double reporting:

- Large overlap between ESRS 2 / IFRS S1 and ESRS E1 / IFRS S2 (governance, risk management, targets, GHG emissions, transition plan).

- N‑ESRS adds impact‑focused requirements (e.g., compatibility with 1.5°C).

Incorporation by reference to the IFRS sustainability report is an option!

What your group should do now (practical preparation plan)

Confirm scope

- Assess EU turnover at group level for the past two years.

- Identify EU subsidiaries/branches with turnover > EUR 200M.

Decide your reporting perimeter

- Global? Mixed? (topic‑by‑topic feasibility assessment) Full ESRS? (if aiming for subsidiary exemption)

Map your current disclosures

- Start from existing sustainability reporting (TCFD, GRI, IFRS S1/S2, local laws…).

- Identify gaps vs. N‑ESRS impact‑focused requirements.

Build or strengthen your due diligence system

- Map and assess actual and potential impacts across entire value chain.

- Document processes, policies, targets, actions and remediation results.

Prepare climate‑related disclosures

- Transition plan aligned with 1.5°C

- GHG inventory (Scopes 1–3)

- 2030 and 2050 targets + progress tracking

Prepare governance & incentives disclosures

- Roles, expertise, oversight mechanisms

- Sustainability‑linked remuneration

Prepare for data collection

- Global data for climate

- EU‑related data for other topics (if mixed approach)

- Value‑chain data (workers, communities, consumers)

Plan for interoperability

- Decide what will be disclosed in the IFRS sustainability report

- Decide what will be incorporated by reference into N‑ESRS

Engage early

- Participate in EFRAG’s consultation and field tests

- Align internal teams (finance, sustainability, legal, operations)

Why N‑ESRS focuses only on impacts (and not risks & opportunities)

-

Article 40a of the CSRD requires transparency on impacts, not financial materiality

The policy objectives of Article 40a are: “Level‑playing field” and “Accountability and transparency of non‑EU companies on impacts”.

This is the legal anchor: The EU wants non‑EU companies to disclose their impacts on people and planet when they operate in the EU market. It is not intended as a full double‑materiality regime for foreign groups.

-

The EU cannot impose financial‑risk reporting on non‑EU parent companies

- ESRS for EU companies are not policy neutral, they support the EU Green Deal and transition agenda.

- The EU can require disclosure of impacts caused by non-EU groups in the EU market.

- But it cannot realistically require a non‑EU parent to disclose global financial risks, opportunities, or resilience assessments.

Thus, N‑ESRS focuses on what the EU can legitimately require from non-EU parent companies: impact transparency, not financial risk analysis.

Requiring non-EU groups to perform full double materiality at global level (including financial risks, opportunities, and resilience analysis) would be disproportionate and legally complex.

You may still mention financial data if it helps explain an impact, but you do not perform the ESRS financial‑materiality assessment.

-

Interoperability with IFRS S1/S2 already covers risks for those who need it

- IFRS S1/S2 = financial risks & opportunities

- N‑ESRS = impacts only

- Overlap exists for climate, but N‑ESRS adds impact‑specific requirements

This separation avoids double reporting and respects the different purposes of each framework.

Want to participate in EFRAG’s field test?

🌿 EFRAG has launched a call for interest to participate in the field test of the draft Non-EU ESRS (N-ESRS) ahead of its public consultation in July 2026. Register here before 1 July and secure direct interaction with EFRAG shaping the future sustainability reporting standard for non EU groups 👉 EFRAG Resumed Work on the European Sustainability Reporting Standard for Non-EU Groups and Launches Field Test Call for Interest | EFRAG

The best way to prepare for N-ESRS reporting? Guided digital ESRS end-to-end templates.

Contact us if you want to use our guided digital ESRS end-to-end templates to get a head start.